SVN Capital Funds letter for the year ended December 31, 2021, discussing their new position in Dino Polska SA (WSE: DNP) and a brief attack on Evolution AB (STO: EVO).

I am positive about the future and excited about our portfolio of services. I continue to remain client and invest with a long period of time horizon.

As I eagerly anticipate 2022, I am reminded of G. K. Chesterton, who stated, “I would maintain that thanks are the highest type of thought, and that gratitude is happiness doubled by marvel.” It is a privilege to serve you. Thank you.

Genuinely,.

Shreekkanth (” Shree”) Viswanathan.

Updated on Jan 7, 2022, 4:54 pm.

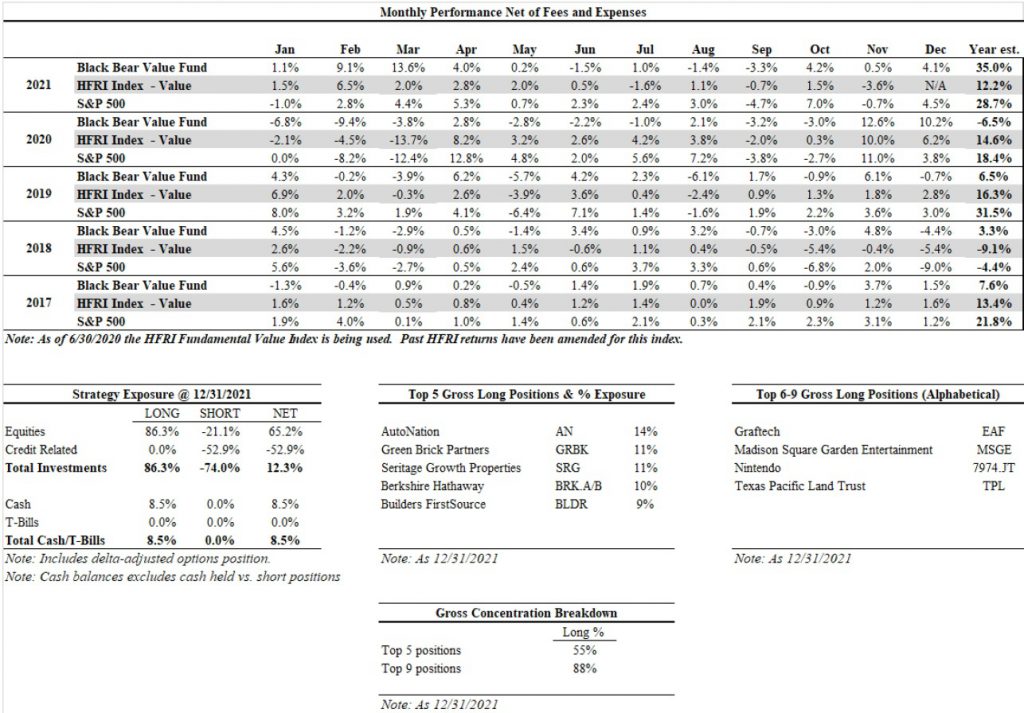

Black Bear Value Fund December 2021 Performance UpdateBlack Bear Value Funds efficiency update for the month ended December 31, 2021. Q3 2021 hedge fund letters, conferences and more Black Bear Value Fund, LP (the “Fund”) returned +4.1%, net, in December and completed +35.0% in 2021. The HFRI index has actually not released their December numbers but was +12.2% through November. The S&P 500 Read MoreDear Partner,

SVN Capital Funds portfolio returned +23.60% gross and +21.09% internet of all costs (topic to audit) for the year 2021. When you invested, your return will be various depending upon.

In the following pages, I will stroll you through changes to the portfolio (which are not substantial), the portfolio composition and description of top quality businesses, a short attack on Evolution AB, and market musings. Prior to I begin with the portfolio, please permit me to digress a bit to discuss the power of persistence unleashed by the Oracle of Buffalo

The Oracle of Buffalo.

While pursuing my research on a Polish business, I stumbled upon a book entitled “The Oracle of Buffalo.” I chose to dig in, and I am thankful I did. A great deal of us have actually heard of the Oracle of Omaha (Warren Buffett). Who hasnt? But have you heard of the Oracle of Buffalo? Stephanie Mucha of Buffalo, NY is that oracle. I think she was just as financially savvy as the one in Omaha.

What was her background? Stephanie was born into abject hardship. Born in 1917 to Polish immigrants Antoni Niciszewski and Mary Strenk, she was one of seven kids. After dropping out of high school, she worked as a housemaid and after that at Buffalo Veterans Medical Center for 44 years as a nurse until she retired in 1994. She got married to Joseph Mucha, a Polish immigrant who was 26 years older than she. By the time Joseph passed away in 1985, the penny-wise couple had actually managed to accumulate a net worth of roughly $469,000.

As a practicing nurse at a VA medical facility, she occurred to come across numerous intriguing products in the medical field. Periodically, if she believed a particular item was appealing, she would do some research study, examine the regulars for any reviews, and speak with her good friends and get their viewpoints before buying some shares in the business.

One day in 1961, she came back from work and informed her husband that she saw a dead pet dog come to life. What she had seen was a presentation of the first implantable cardiac pacemaker by Medtronic (MDT). Joseph and Stephanie Mucha bought 50 shares of Medtronic at $5.11 per share for an overall of $255.50. And here is the kicker … In 2007, when she contributed a part of the shares, she had 8,500 shares as a result of stock divides and dividend reinvestments at $66.00/ share for a total of $561,000. A little investment of $255.50 had grown at 2,200 x over 46 years.

She purchased shares of Pfizer, Merck, Abbott, Johnson & & Johnson, Bayer, and GlaxoSmithkline and unleashed the magic of patiently intensifying her capital resulting in $3.0 million by 2007. By the time she passed away in 2018 at the age of 101, she had become an effective philanthropist, distributing roughly $6.0 million to a few of her favorite causes and institutions.

What was the secret to her success? It was a combination of economical living and a distinct method to investing– purchasing stocks of particular services whose items she liked and sitting on them … for decades. I too mean to unleash such patience on our portfolio.

Stephanies financial investment style resonated well with me. A patient, long-lasting approach is one of my core tenets at SVN Capital. I look to purchase and hold a choose few openly traded businesses that satisfy the following four investment criteria– services that:

I comprehend;

not only generate a healthy return on incremental capital but also have great reinvestment chances;

are run by sincere and proficient management teams with “skin in the video game;” and

are trading at a sensible assessment.

Dino Polska S.A. (” Dino”) – A New Investment

The only brand-new financial investment I made in the second half of 2021 was Dino Polska SA (WSE: DNP), a grocery chain in Poland. In September 2021, I discussed Dino, which you can discover here.

Among the special aspects of our fund is the ability to purchase great companies worldwide. While Poland is a former communist nation, it has actually grown at a constant 4.0% approximately over the last 30 years to be the 6th largest economy in the EU. And yet, unlike other fast-growing countries, backwoods of Poland are not clearing into the cities. The urbanization rate in Poland is low compared to other developed and fast-growing nations. Practically 60% of the population of ~ 40 million reside in rural areas and villages with less than 50,000 people. This fact works splendidly for Dino, which focuses on rural areas.

Durable and strong competitive strength is what helps an organization defer the typical ailment of “reversion-to-the-mean” returns that most organizations face. With just 4 shops per 100,000 people throughout the country, I believe the business can quickly double its existing store base of 1,700 by 2025.

Such durable development managed by a qualified group with skin in the video game, that has actually chosen to reinvest all its totally free cash circulation back into growing its store base, makes Dino a special investment opportunity. For more details click the link above.

Portfolio

We currently own 10 financial investments. Money is roughly 5.3%. A picture of the portfolio since 12/31/21 is in Appendix I.

Our portfolio is a collection of top quality organizations. The cash conversion rate of our portfolio is 84% vs. 75% for S&P 500 companies.

Debt/Equity of our portfolio is just 23%, while that of S&P 500 companies is much higher. Interest protection for our portfolio is nearly 10 times that of S&P 500 business.

As I have actually revealed above, our portfolio of businesses is essentially far much better than the average; it creates more cash, is capital effective, and brings little in terms of financial obligation, yet it trades at a comparable assessment as the market.

The leading 5 holdings account for roughly 62% of the portfolio. 48% of our portfolio is noted in the US, while the rest is spread out among Poland, Sweden, Israel, and Italy.

Return on Invested Capital (ROIC) is the primary test of performance in handling a company. Not only do our companies generate high returns on capital, but they likewise have terrific opportunities to reinvest in their own businesses. The combined results of high returns and high reinvestment rate over a long stretch of time results in considerable growth in intrinsic value.

Over a time period, complimentary cash circulation development will drive market price growth. Healthy free money circulation development is likewise a terrific gauge of corporate health. FCF growth of our portfolio is nearly two times that of the S&P 500 index.

The capital strength of our portfolio is simply about 1/3rd of the markets. The capital performance of our portfolio is about two times that of markets.

A high cash conversion rate reveals the managements ability to effectively convert its profits into money, as well as provide versatility with respect to its usage– reinvest in the business or return it back to debtholders or shareholders. The money conversion rate of our portfolio is 84% vs. 75% for S&P 500 companies.

Our collection of high-quality companies brings low financial take advantage of. Given that I seek to own these investments for a very long time, I choose to own businesses that carry low financial debt, due to the fact that the higher the financial utilize, the more unstable will be the returns in time. Debt/Equity of our portfolio is only 23%, while that of S&P 500 business is much higher. Associated with the level of financial obligation is interest protection, which reveals the relationship in between profits before interest and the interest charge. A high ratio suggests financial stability and versatility at the very same time. Interest coverage for our portfolio is nearly 10 times that of S&P 500 companies.

The last concern is about valuation. The free cash flow yield (next years free cash flow/enterprise value), a primary assessment metric I use, of our portfolio is roughly 3.5%. Incidentally, the S&P 500, which is a good reflection of the general market, is likewise trading at the exact same appraisal. As I have actually revealed above, our portfolio of organizations is essentially far better than the average; it generates more money, is capital efficient, and carries little in terms of debt, yet it trades at a similar valuation as the market. I highly think that our portfolio is attractively priced.

A Short Attack on Evolution AB (EVO).

On November 19, 2021, after the market closed, a lawyer in New Jersey, acting on behalf of the author or sponsor, released an anonymous 121-page brief report on Evolution AB, one of our portfolio holdings (I initially wrote about EVO here). Within a matter of 10 trading days, the stock was down by 40%. With EVO being the biggest position in the portfolio, it harmed like a thumb on the getting end of a slamming door– swift and sharp.

Accusations.

Obviously, the report was sponsored by one of EVOs US competitors. It had worked with a player to discreetly pierce the security infrastructure of the company with the sole intent of soiling the companys track record.

EVOs video games can be accessed not only from jurisdictions that have actually made such games unlawful (e.g., Singapore), however also from unsanctioned horror states that are prohibited by the US (e.g., Iran and Syria). It likewise declared that EVO is mindful of such transgressions, yet allows them to continue.

Gaming regulators in New Jersey had actually been alerted and, because of the seriousness of security lapses, they are likely to cancel EVOs license to use its video games in New Jersey.

Background.

Before I unpack the details, let me provide some context.

Advancement offers the entire infrastructure required to run an online casino, especially video games with a live dealer. For example, when a consumer of DraftKings based in one of the 5 states that currently enable online betting (CT, MI, NJ, PA, and WV) desires to play blackjack or roulette with a live dealer, Evolution is the company making it occur in the background. Considering that it is an online video game supplier, it has online access blockers for preventing access from specific jurisdictions. The ultimate duty of executing such blocks lies with the operator (e.g., DraftKings).

One of the most significant growth chances for the company is North America, especially the US, where it is a dominant provider. While Nevada sets the regulatory tone for land-based casinos, within the US, New Jersey sets the tone for online casinos. The possibility of New Jersey regulators penalizing EVO and canceling its licenses caught the fancy of many financiers and financial press, particularly in Sweden where it made the front pages of regional papers.

Response … Sort Of.

The speed at which incorrect information was spreading reminded me of Mark Twain, who said, “A lie can travel halfway around the world prior to the reality puts on its shoes.” Beginning Monday, November 22, 2021, the stock without delay started moving and got in ferocity as days progressed … with hardly any action from the business. Even though EVO was the biggest position in the portfolio, I saw the weakness as a chance to buy more.

On November 24, 2021, the company launched a one-page rebuttal of some of the claims in the report. At the exact same time, he accessed a web address in Germany through which he was able to access Evolutions games.

The one-pager likewise said that they work closely with the regulators to continuously enhance its operations. The company had actually proactively reached out to the regulators in New Jersey and had actually initiated an internal evaluation. In addition, the one-page rebuttal also said that EVO would hold a conference call.

While the release was helpful in clarifying some of the questions, it left numerous questions unanswered. The market saw managements uncertainty as “where there is smoke, there need to be fire,” and sent the stock down another 15% the next day. I purchased some more EVO.

My Reaction.

While I was dissatisfied with managements inadequate one-page counterclaim and for not having actually opened up the call for Q&A, I agreed with them that the supreme duty of enabling or prohibiting a player lies with the operator. For a regulator to punish Evolution in such a circumstance would belong to penalizing Budweiser for an alcohol shop that sold beer to a minor who forged his identity.

I stayed confident that Evolution was, is, and will be a dominant business in the online gaming market. It is run by a competent management team, monitored by a board where the 2 original creators of the company sit. In spite of EVO being the biggest position in the portfolio, my reaction was to buy more on the way down.

Mistakes Compound Too.

The management groups naivete led to some mistakes, which then intensified soon thereafter. While it is typical in the US to use an investment bank and/or PR firm to prepare an action in similar scenarios, the management group naively chose to handle it with internal resources.

Not only did the choice lead them to not open the call for Q&A, however it manifested in the one-page release. The last sentence in the release read, “An internal review has actually been started to guarantee a swift response to any questions from the NJDGE [New Jersey Division of Gaming Enforcement]” To an American financier, the phrase “an internal evaluation has been started …” implies a recognition of something wrong. What the business suggested was, “we will make certain to respond in a timely fashion.” Too late. The damage had been done.

With respect to the relationship with regulators, the management team described in excellent detail how the business is in routine contact with regulators around the globe and how it adheres to all regulator demands. While he didnt wish to promote the regulators, he didnt believe there was any benefit to the accusation that NJDGE is likely to penalize the business. Having worked in a bank earlier in my career, I could relate to how the business would work hand in glove with the regulators to prevent any surprises. It would have been nice to hear this from the CEO of the business. Too bad they didnt open the call for Q&A.

Reaction … V2.

On December 2, 2021, by which time the stock had actually declined by approximately 40%, the business revealed a Eur 200 million share bought program. This was the first genuine self-confidence booster from the management group. It assisted stem the tide a bit.

Martin covered a wide range of topics including the regulative landscape, unregulated markets, aggregators and operators, payments, and the share bought program. He was also excited about 2022, when EVO anticipates to launch more games.

So, What Now?

Having actually realized their follies– not performing an extensive Q&A session, not taking professional assistance in preparing a response to the brief attack, and using a specific expression in the press release that raised much more questions– the management team has actually been hectic responding to questions behind closed doors, calming worries. Also, the business repurchasing Eur 122 countless shares is another strong signal. The stock has actually recuperated much of its early losses however is still around 15% lower than where it was on November 19th, before the brief report was released.

While the businesss handling of the matter has left a lot to be preferred, my self-confidence in business design and the management groups operating know-how remains high. In truth, having actually discovered more about the regulatory landscape, my self-confidence has actually just increased. I more than happy to have actually gotten some more shares of EVO throughout the height of the panic. For many years, I am confident that this event will prove to have actually been a great buying opportunity, and I expect to make lots of multiples on our financial investment in EVO.

As I cover up this section, I am reminded of a comment by Charlie Munger who stated, “… bearishness and drawdowns of 40– 50% are the price of admission for being an investor which everybody goes through it.” It is one of the crucial reasons I focus on high-quality organizations; because, gradually, they are much better able to endure such hits.

Market Musings.

In the mid-year 2021 letter, I stated, “Inflation is the existing bugaboo as it connects to investing.” It continues to be so. As I compose this letter, the monetary media, with its deep commitment to terrifying everyone out of the equity market, is pointing to how the Consumer Price Index (CPI) has actually soared 6.8% from a year previously. The last time inflationary pressures were this high remained in 1982. The concern now seems to be not if inflation is here, but is inflation temporal, or is it here to stay.

Yes, the heading reads “inflation is at a 40-year high,” but is it here to remain? I am not so sure. While the stock exchange has been choppy, the bond market doesnt appear to care much. For instance, rates of interest are still languishing around lowest levels, while they were practically at all time highs in 1982. Similarly, the USD is sending out a different signal; if stagflation impended, the USD would be heading south … in a hurry. DXY, a fund that tracks the USD, just recently hit a 16-month high.

I am convinced that the economy can not be consistently forecast, nor the marketplaces consistently timed. I think that the only trusted method to capture the complete long-lasting return of equities is to ride out their short-term but regular declines.

As I recall at 2021, and particularly the volatile last couple of months due to inflation worries, or the brand-new variant of COVID-19, I am reminded of a wonderful book by Nick Murray, “Simple Wealth, Inevitable Wealth.” In it he captures the essence of the book and his investment philosophy in a postcard, part of which I have actually recreated listed below. It succinctly captures my investment viewpoint at SVN Capital, also, especially # 2, “Dont panic: the secret to wealth in equities is not getting terrified out of them.”.

Of course, what matters is not where these business are noted, however where they create their earnings and sustain costs. In aggregate, our portfolio companies produce approximately 50% of their income in North America, while the rest is geographically spread out a lot more commonly than the nations noted above.

Our portfolio is a collection of premium businesses. The following table notes some of the essential metrics of our portfolio and the S&P 500 index, which is a great reflection of the general market. Our portfolio metrics are materially better than the market.