After A Tough Year, Odey Asset Management Finishes 2021 On A HighFor much of the past decade, Crispin Odey has been awaiting inflation to rear its ugly head. The fund supervisor has been placed to make the most of rising prices in his flagship hedge fund, the Odey European Fund, and has been attempting to alert his financiers about the dangers of inflation through his annual Read MoreHistorically Negative Combination

Making complex things is a rise in inflation that is likely to continue through these waves as decades of simple cash policy, of lower labor share of wealth/income and now the worldwide disruptions connected with the infection will press costs up. That suggests that we will require to handle through a period of lower development and greater inflation. Historically that is an extremely unfavorable mix for asset rates.

The peak of the first wave appeared in the 3rd quarter monetary declarations database update that was simply finished. The frequency of rising sales development and increasing gross profit margins was lower in the period and it is those frequency numbers that typically mark the development peak.

Rising Inflation And Interest Rates

The only way to defend our assets from the negative affect of increasing inflation and interest rates is to own speeding up business. Just increasing growth will provide defense against rising rate of interest. The rebound from the infection depressed levels in 2015 has most business taping velocity attributes.

Just recently, the biggest rebound was the energy group where sales growth dropped to -50% (at the most infection depressed duration) but has given that recuperated to 44% in the current update; with a massive 88% of energy companies accomplishing an improvement.

Oil & & Gas Cycles

There are a number of cycles in our data record but in a normal oil and gas cycle we would start to see a velocity in capital investment as business respond to greater oil rates with bigger exploration and advancement spending. Effectively executed brand-new projects would change fading production in other places and contribute to provide growth.

Recent proof recommends the opposite is occurring in the oil and gas market. Capital expenditures continue to fall relative to sales. Oil costs continue to advance, production is fading but not being changed and supply development is slowing.

Energy Demand Continues To Grow

The world is not willing to minimize energy use. There is incredible resistance to higher oil costs and lower fuel-cost subsidies as we have seen in social discontent duplicated in recent years. A lot of recent example in Kazakhstan.

Econ 101

Higher energy costs and carbon taxes will sustain high inflation. The current yield on long term bonds is 2% producing an after inflation (real) negative return of -5%!

Back In 1979.

The last time (1979) inflation was behaving in this trend, long treasury bonds yielded 12% for a real return of 5%. The rate of long treasury bonds would fall by over 80% if Bond yields were to increase to 12% now. This is an approaching retirement disaster.

Terribly crucial to retirees, please review your retirement accounts now and sell all fixed earnings securities. The only way to protect our properties from the negative affect of increasing inflation and rate of interest is to own speeding up companies. Only increasing development will supply defense versus increasing interest rates. The rebound from the virus depressed levels in 2015 has most companies recording velocity qualities.

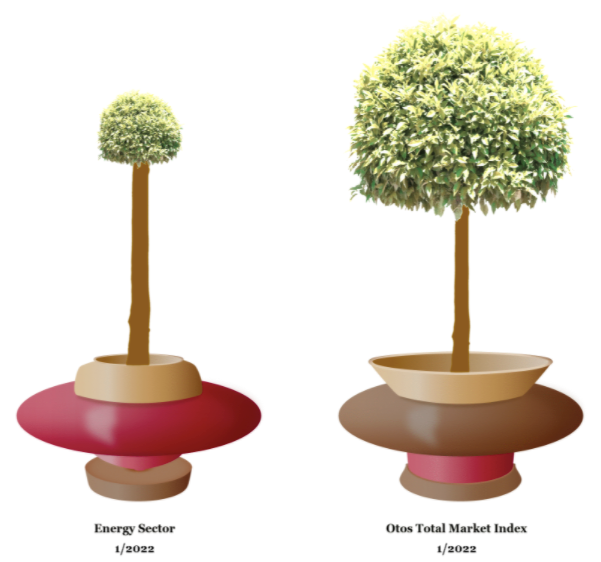

Otos MoneyTree

Otos display screens rising sales development and increasing profit margins as a MoneyTree with a green globe, a dark trunk, and a golden pot. As companies report their monetary statements in coming weeks, be scrupulous around the growth attributes of your portfolio companies.

Whatever Quantitative Tools you choose to use, your portfolio of business must have rising growth characteristics (MoneyTree with a green world, dark trunk and hourglass shaped golden pot).

The present Otos Total Market Index portfolio MoneyTree below has high and rising sales growth, increasing profit margins and high operating/financial take advantage of.

Choose Active Portfolio Management and validate that your portfolio qualities are, put simply, growing!

SEC Filings Of Annual Reports

This is the last update of the 3rd quarter financial declaration update with the Securities and Exchange Commission (SEC) however soon updates from the 4th quarter year-end duration will begin. Many business will quickly to be reporting their yearly period ended December. The reporting deadline for yearly monetary statements is later so it will be early March before we see a full macro picture (stay tuned).

All the best in 2022 and make sure!

Happy New Year friends and financiers! What an incredible new year it is most likely to be. Like a bolder dropped in a pond, the infection produced a substantial implosion of corporate growth in 2020 and an extraordinary surge of development in 2021. Extending the ripple-in-a-pond metaphor we might expect that these waves will diminish in magnitude and then settle. When and how rough will the waves be in 2022? And which sector( s) will possibly be triggering it.

Updated on Jan 17, 2022, 3:53 pm

Like a bolder dropped in a pond, the virus produced a huge implosion of corporate growth in 2020 and an unmatched explosion of development in 2021. That implies that we will require to handle through a period of lower growth and higher inflation. Only increasing growth will offer defense versus rising interest rates. Oil costs continue to advance, production is fading but not being changed and supply growth is slowing.

Only increasing development will provide defense versus rising interest rates.